The COVID-19 economic shutdown and emergency spending measures have caused government debt in Canada to balloon. The most recent estimates suggest that, at the federal level alone, the deficit for 2020-21 will be in the range of $343 billion. In just one year, Ottawa will have added more debt than it did in the last 20 years combined.

Source: Government of Canada, Fiscal Reference Tables September 2019, projections from Economic & Fiscal Profile: Covid-19 in Canada

The situation is no different at the provincial level. Here in Alberta, the budget deficit was initially estimated to be around $6 billion but, as of most recent estimates from Alberta’s fiscal update, is expected to be closer to $24 billion.

The challenge will not go away any time soon. A gradual recovery, extended income support programs, and stimulus spending to get the economy going again will mean large deficits are in the cards for years to come.

And finally, the resignation of former Finance Minister Bill Morneau has caused added concern in some circles. Reports suggest that the Finance Minister had ‘clashed’ with Prime Minister Justin Trudeau over soaring government spending, with one insider saying he was ‘alarmed by ballooning deficits’. Their worry is that Morneau was the voice of fiscal temperance in the federal Cabinet and that his departure removes a key barrier to even more unfettered spending.

But how much of a problem is government debt, really? And should Canadians be worried?

Bottom line: Is the current level of debt a problem? Not yet. Moving forward, what matters most to the government’s bottom line will be the strength of the economic recovery.

This commentary takes a closer look at government borrowing and what it could mean for our long-term prosperity.

How did we get here?

How we got here is pretty clear. The COVID-19 economic shutdown caused government tax revenues to plunge, while emergency income and business supports added hundreds of billions of dollars to expenditures.

The Business Council of Alberta supported those emergency spending measures at the time. They were the right thing to do for an economy in an unprecedented shutdown. And because of that spending, the impact was far less severe than during, say, the Great Depression. Not that there hasn’t been adversity, but absent generous government income and business supports, the picture in Canada would have looked more similar to the one painted in Dorothea Lang’s Migrant Mother. Incomes would have plummeted, more businesses would have closed, and the short-term shutdown would have turned into enduring hardship.

The downside, however, is that Canada has accumulated a massive amount of debt in a very short period of time. Not only that but in a traditional fiscal policy sense, we have very little to show for it. That debt did not buy us any new assets or create a more competitive economy. To use a household analogy, Canada did not borrow money to buy a car or a house; it borrowed money to pay for food and utilities.

How does the government borrow and from whom?

Keeping with the household analogy, it’s easy to think of government borrowing in terms of taking out a loan. You borrow money from the bank to pay for tuition or a car and then pay back the principal plus interest over time.

It actually works a little differently for governments. When governments borrow, they do so by selling thousands of individual ‘IOUs’—referred to as Treasury bills (T-bills) or bonds, depending on the timeline for repayment. Each bond or T-bill specifies the amount to be repaid and when. With varying due dates, there is a continual rollover of government debt. When one bond expires and needs to be repaid, the government will simply replace it by issuing another.

Government bonds are considered to be one of the safest assets, mostly because governments have the power to tax. They can tap into a large reserve of cash from individuals and businesses at any time. There may be long-term economic consequences for doing so, but the important part is that they can do it if they need it. As a result, governments generally can ask for low interest rates when they borrow, and lenders are generally confident they will be paid back plus interest by the agreed-upon date.

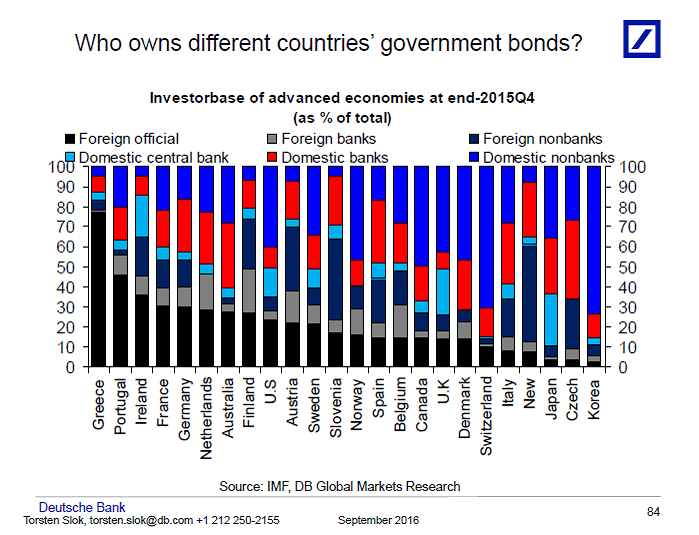

Currently, most of Canada’s debt is held by individuals and businesses in Canada, with the rest held by banks and foreign investors.

{kind=link}

Is the resulting deficit and debt cause for concern?

Not yet. But we have some important decisions ahead.

In total, Canada’s total gross government debt was about $2 trillion pre-COVID-19. The additional borrowing as the result of COVID-19 will bring Canada’s total debt to around $2.4 trillion, or about $64,000 per person.

It’s worth noting that governments and media outlets often report much lower numbers. Those figures represent net debt, where governments subtract the value of financial and non-financial assets from gross debt. Using Alberta as an example, it would be like subtracting the value of the Heritage Fund and provincially owned roads from our debt because those things could, theoretically, be sold to pay down the debt.

We focus on gross debt here because of some flaws with the concept of net debt and for ease of international comparisons.

Source: IMF

These may sound like huge numbers, but it’s not quite as bad as it looks. How manageable a given amount of debt is depends on the size of a country’s economy. To measure this, economists often use what is called the debt-to-GDP ratio, a ratio of the total amount of money owed by the government to the value of the economy as measured by GDP. Going back to our household analogy, this is like measuring your credit card debt as a percentage of your household income; a $5,000 credit card balance is a lot more of a problem if you make $10,000 a year than if you make $150,000.

Research from the World Bank concluded a 77% debt-to-GDP ratio is the threshold beyond which debt will inhibit economic growth. This conclusion is based on two broad ideas: the percentage of government revenues dedicated to paying interest on that debt; and the risk that government borrowing will ‘crowd out’ investment in the private market. Research by central banks concluded the threshold might be closer to 85%. However, Harvard Economists Jason Furman and Lawrence H. Summers write, “In truth, no one knows the benefits and costs of different debt levels—75 percent of GDP, 100 percent of GDP, or even 150 percent of GDP”.

Moreover, the economic consensus on government debt is evolving, especially in light of COVID-19. The Economist notes, “Even economists with reputations as fiscal hawks tend to support today’s emergency spending”. This idea was further supported in a survey of the most conservative economists. Slowly, the old ideology of placing balanced budgets as a top priority has given way to more flexible views of spending and debt.

Pre-COVID, Canada’s total gross debt-to-GDP ratio was already about 88%. While that larger number is within the danger zone cited above, when compared with other G7 countries, Canada’s debt levels seemed relatively reasonable.

Source: IMF

Source: IMF

Post-COVID, estimates suggest we will see as much as an 18-percentage point increase in the federal debt-to-GDP ratio. Adding provincial debt, this means the total government debt-to-GDP ratio will likely increase to over 106%. This would be the highest debt-to-GDP ratio we have seen in at least 20 years and certainly beyond the point where economists previously expected government debt to begin to inhibit economic growth.

But the debt-to-GDP ratio overlooks one important factor: the cost of borrowing money. How much the government pays is not just a factor of how much it borrows (i.e. the total debt) but also of what interest it must pay. Canada needs to be able to repay lenders as bonds come due without significantly cutting into other government spending or piling on more debt.

Fortunately, interest rates are so low that even a large amount of debt is relatively cheap for the government to finance. This means that while the total debt and the debt-to-GDP ratio will rise considerably, the government could end up paying less servicing that debt and still well below the 20 cents of every $1 dedicated to debt payments in the 90s.

To put this in perspective, the interest rate on a 3-year bond decreased from about 1.44% to just 0.27%; that’s just one-fifth of the old price. What’s more, in the 90’s, it would have cost 30 times this to borrow the same amount, with an interest rate of about 9%.

Source: Bank of Canada

Source: Bank of Canada

What is the biggest concern?

Policy decisions made by the Bank of Canada have helped to make it cheap for the government to borrow. The biggest concern moving forward is that interest rates will increase, making debt payments much heftier for the government to manage. This would ultimately require a major increase in taxes or cuts in future spending.

One way this could be triggered is if prices begin to rise enough as economic activity rebounds that the Bank of Canada must respond by increasing interest rates to curb inflation. In turn, this would make it more expensive for the government to continue to make its debt payments.

Though introductory economics textbooks espouse this logic, empirically it does not always hold. One recent example is the lack of inflation in the US following the near $1 trillion dollars of fiscal spending and tax cuts in response to the Great Recession.

Where do we go from here?

What matters most is where we go from here.

Canada has two ways to work its way back to pre-COVID levels of debt, to ensure we do not have to sacrifice welfare for debt payments for years to come.

The first, and most obvious, is to cut spending and/or increase taxes. In the current context, government spending will be hard to cut, with individuals still getting back on their feet, big pushes for green investment to tackle climate change, continued health and safety concerns, and an aging population. Furthermore, cutting spending to eliminate deficits could come at the expense of a speedy recovery. This would, ironically, have a greater, more lasting impact on government debt.

Similarly, an increase in taxes could backfire if it hurts consumer spending, increases bankruptcies, and limits investment. It also ignores the fact that a large part of the deficit is explained not just by additional spending but due to lost revenue in taxes. In short, great harm can be done in reducing the deficit.

Another way for Canada to decrease debt is to ‘grow its way’ out of it. Though it might sound too good to be true, history shows it is possible when recovering from a tragedy. Canada pulled its way out of WWII debt thanks to low interest rates and a booming economy. As written in The Economist, “If interest rates remain lower than nominal economic growth—ie, before adjusting for inflation—then an economy can grow its way out of debt without ever needing to run a budget surplus.”

To do this, all spending moving forward should be determined by the severity of the crisis and viewed through a lens of whether it enhances Canada’s competitiveness and productivity and enables long-term growth. If it is not, markets will be quick to give feedback, letting us know we are headed for a low-growth/high-debt payment future if we do not correct course.

Note: This commentary does not assess the impact of the COVID-19 shut-down, recession, and economic recovery by race or ethnicity, another important factor to consider beyond gender. Statistics Canada just recently began collecting data on race and ethnicity as of July. In future commentaries, we will dig into these important differences, once more data become available to better understand the relative trends and impact for different groups.

[poll id=”2″]